🔑 Key Takeaways

- Mortgage points (also called discount points) let you pay upfront cash to lower your interest rate — typically 0.25% per point on a $100,000 loan increment.

- The break-even analysis is the only honest way to decide: divide your upfront cost by your monthly savings to find out how many months until paying points actually pays off.

- If you plan to sell or refinance before reaching your break-even point, buying points is almost always the wrong move — regardless of how good the rate looks on paper.

- No-points mortgages preserve your cash at closing, which matters enormously for first-time buyers and anyone keeping reserves for repairs, moving costs, or emergencies.

- The right answer depends on your specific numbers, your timeline, and your financial situation — not on what sounds better in a lender's pitch.

- In the Dallas-Fort Worth market, where home prices and loan amounts are significant, even small rate differences can produce large long-term savings — or large upfront costs. The math matters.

You're sitting across from a lender — or maybe staring at a loan estimate on your screen — and there it is: the option to buy points. The lender says something like, "For just a little more at closing, you could lock in a lower rate for the life of the loan." It sounds reasonable. Maybe even smart. But something in you hesitates, and you're not sure whether that hesitation is wisdom or just nerves.

That hesitation is worth listening to.

The decision to buy mortgage points — or skip them entirely — is one of the most consequential financial choices in the home buying process, and it's also one of the least clearly explained. Most buyers either accept the points without running the numbers, or reject them without understanding what they're giving up. Neither approach serves you well.

This guide is going to slow that decision down. We're going to look at exactly how mortgage points work, walk through a real break-even analysis using actual numbers, and help you figure out which path makes sense for your situation — not someone else's. Whether you're buying your first home in the Dallas-Fort Worth area or you're an experienced buyer refinancing into a better rate, this is the kind of clear-eyed breakdown that should have been in front of you from the start.

What Mortgage Points Actually Are (And What They're Not)

Let's start with the basics, because the word "points" gets used loosely in ways that can genuinely confuse people.

A mortgage point is equal to 1% of your loan amount. On a $400,000 loan — which is squarely in the range for a lot of DFW buyers right now — one point costs $4,000. Two points cost $8,000. That money is paid at closing, upfront, in addition to your down payment and other closing costs.

In exchange for paying that upfront cost, your lender reduces your interest rate. The exact reduction varies by lender and by market conditions, but a common rule of thumb is that one point lowers your rate by approximately 0.25%. So if your baseline rate is 7.00%, buying one point might bring it to 6.75%, and buying two points might bring it to 6.50%.

💡 Quick Explainer: Points vs. Origination Fees

There are actually two types of "points" that show up on loan estimates, and they are not the same thing. Discount points are what we're discussing here — you pay them voluntarily to buy down your rate. Origination points are fees the lender charges for processing your loan. Origination points don't reduce your rate; they're just a cost of doing business with that lender. Always ask your lender to clarify which type of points appear on your loan estimate, because they serve completely different purposes.

It's also worth noting that points are tax-deductible in many situations. If you're buying a primary residence and you meet IRS requirements, discount points paid at closing may be fully deductible in the year you pay them. This can meaningfully change the effective cost of buying points, particularly for buyers in higher tax brackets. That said, tax situations are individual, and you should confirm this with a tax professional before factoring it into your decision.

Now, here's where it gets interesting: the fact that points reduce your rate doesn't automatically mean they're a good deal. Whether they make financial sense depends entirely on one number — your break-even point. And that's what most lenders don't walk you through clearly.

Understanding the No-Points Mortgage: What You're Choosing Instead

When you choose a no-points mortgage, you're accepting a higher interest rate in exchange for keeping more cash in your pocket at closing. That's the trade. The question is whether that trade is worth it for your specific situation.

A no-points mortgage isn't a compromise or a consolation prize — for many buyers, it's the strategically smarter choice. Here's why:

First, closing costs are already substantial. In Texas, buyers typically pay between 2% and 5% of the loan amount in closing costs. On a $400,000 purchase, that's $8,000 to $20,000 before you've even considered points. Adding another $4,000 to $8,000 for points can stretch your cash reserves dangerously thin — especially if you're also putting down 3.5% to 10% on an FHA or conventional loan.

Second, that cash has alternative uses. The $4,000 you'd spend on one point could instead sit in your emergency fund, cover your first year of HOA dues, handle a repair that comes up after move-in, or simply give you breathing room while you settle into homeownership. For first-time buyers especially, liquidity matters more than people realize in those first twelve months.

👍 You're Not Wrong to Feel Uncertain About This

A lot of buyers feel like they should just "know" whether to buy points — like it's obvious and they're missing something. You're not missing anything. This decision is genuinely nuanced, and the right answer depends on numbers that are specific to you. The fact that you're pausing to think it through is exactly the right instinct.

Third, the no-points path gives you flexibility. If rates drop significantly — which they have done historically in cycles — you may want to refinance within a few years. If you've paid points on your current loan and then refinance before hitting your break-even point, you've essentially thrown that upfront money away. A no-points mortgage keeps your options open without a sunk cost hanging over future decisions.

The no-points mortgage isn't about settling for a worse deal. It's about recognizing that the "better" rate isn't actually better if you don't stay in the loan long enough to recoup what you paid for it.

Trying to figure out what your actual numbers look like before you sit down with a lender? Understanding how your loan amount, rate, and timeline interact can save you thousands — and we're happy to walk through it with you.

Talk Through Your Numbers With UsThe Break-Even Analysis: The Only Math That Actually Matters

Here's the core of the entire points decision, and it's simpler than most people expect. The break-even analysis answers one question: How long does it take for the monthly savings from a lower rate to equal the upfront cost of buying that rate down?

Once you know that number — your break-even month — the decision becomes much clearer. If you plan to stay in the home and keep the same loan longer than the break-even period, buying points likely makes sense. If you expect to sell, move, or refinance before that point, it probably doesn't.

Let's work through a real example using numbers that are realistic for the DFW market.

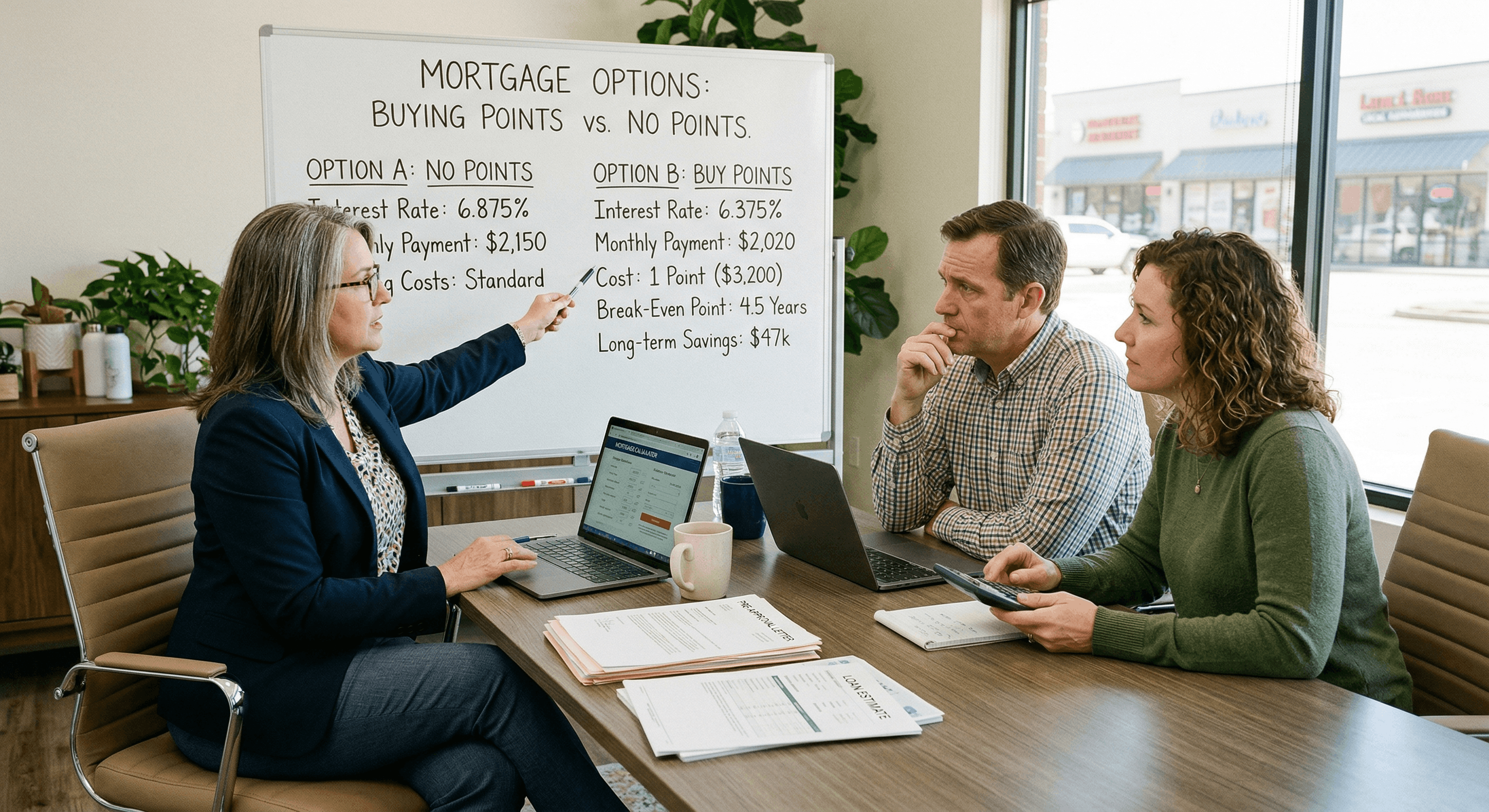

📈 Break-Even Scenario: $400,000 Loan, 30-Year Fixed

Option A — No Points: Interest rate of 7.00%

Option B — One Point ($4,000 upfront): Interest rate of 6.75%

Monthly payment, Option A (principal + interest): $2,661

Monthly payment, Option B (principal + interest): $2,594

Monthly savings from buying the point: $67

Break-even calculation: $4,000 ÷ $67 = approximately 60 months (5 years)

Conclusion: If you stay in this loan for more than 5 years, buying the point saves you money. If you sell or refinance before month 60, you lose money on the deal.

Now let's look at a two-point scenario, because some buyers are offered deeper buydowns:

📈 Break-Even Scenario: $400,000 Loan, Two Points

Option A — No Points: Interest rate of 7.00%

Option C — Two Points ($8,000 upfront): Interest rate of 6.50%

Monthly payment, Option A (principal + interest): $2,661

Monthly payment, Option C (principal + interest): $2,528

Monthly savings from buying two points: $133

Break-even calculation: $8,000 ÷ $133 = approximately 60 months (5 years)

Conclusion: Interestingly, the break-even period is similar — but the total savings after year 10 are dramatically higher with two points ($7,980 in savings vs. $4,020 with one point), and after 30 years the difference is enormous.

This is why the break-even analysis matters so much: it reveals that the upfront cost scales with the savings, and the timeline is the real variable. Two buyers with identical loans can make completely opposite correct decisions based solely on how long they plan to stay.

"The question isn't whether buying points is a good deal in the abstract. The question is whether it's a good deal for you, in your situation, with your timeline. Those are very different questions."

Long-Term Savings: What the Numbers Look Like Over 10, 20, and 30 Years

The break-even analysis tells you when you start saving money. But the long-term savings picture tells you how much you ultimately save — and over a 30-year mortgage, the numbers can be striking.

Let's return to our $400,000 loan and look at what happens across different time horizons:

| Scenario | Upfront Cost | Rate | Savings at Year 5 | Savings at Year 10 | Savings at Year 30 |

|---|---|---|---|---|---|

| No Points (7.00%) | $0 | 7.00% | Baseline | Baseline | Baseline |

| One Point (6.75%) | $4,000 | 6.75% | $20 net loss | $4,020 net savings | $24,120 net savings |

| Two Points (6.50%) | $8,000 | 6.50% | $20 net loss | $7,980 net savings | $47,880 net savings |

These numbers assume you keep the same loan for the full period without refinancing. In practice, the average American refinances or moves roughly every 7-10 years, which is why the 10-year column is often the most realistic benchmark for long-term planning purposes.

What stands out here is that the long-term savings from buying points are genuinely meaningful — nearly $48,000 over 30 years for a two-point buydown. But the 5-year picture is almost neutral, which underscores why the break-even timeline is so critical. If you're confident you'll be in this home for 10+ years, the math starts to favor buying points. If you're uncertain about your timeline, the no-points path protects you.

💰 Don't Forget the Opportunity Cost

Here's a layer most people miss: the $4,000 or $8,000 you'd spend on points could be invested instead. If that money earns even a modest 5-6% annual return in an index fund or high-yield savings account over 10 years, it grows to roughly $6,500 to $13,000. That's real money that competes with the savings from a lower rate. There's no universally right answer here — it depends on your investment habits, risk tolerance, and how confident you are in your timeline. But it's worth factoring in.

When Buying Points Makes Sense: The Right Buyer Profile

Buying mortgage points isn't universally smart or universally foolish. It's situationally appropriate — and understanding the profile of a buyer for whom points make sense helps you assess whether that's you.

Points tend to be a strong financial move when:

- You have a long, stable timeline. If you're buying a forever home — or at least a home you're confident you'll stay in for 10 or more years — the long-term savings from a lower rate can be substantial. The longer you stay, the more you save, and the more the upfront cost becomes irrelevant relative to the total interest savings.

- You have cash reserves after paying points. This is critical. Buying points should never leave you financially exposed. If you can pay the points and still maintain 3-6 months of living expenses in reserves, the upfront cost is manageable. If paying points would drain your savings, it's not the right move regardless of the math.

- Rates are relatively high and you don't expect to refinance soon. When rates are elevated — as they have been in 2023 and 2024 — locking in a lower rate through points can be particularly valuable, especially if you believe rates will stay elevated for several years. If you think rates will drop significantly and you'll refinance within 2-3 years, points are a poor bet.

- The seller is offering to pay your points. In a buyer's market or a negotiated transaction, sellers sometimes offer concessions that can be used to buy down your rate. This is essentially free money — if a seller is willing to pay 1-2 points on your behalf, the break-even calculation changes completely because your upfront cost is zero.

- You're on a fixed income or tight monthly budget. For buyers where the monthly payment difference is meaningful — say, $67 to $133 per month — a lower rate can make a home genuinely more affordable month to month, even if the break-even takes five years. Sometimes cash flow matters more than the long-term math.

Curious how the DFW market affects your specific buying strategy right now? Understanding what sellers are offering in concessions — and how to negotiate points into your deal — is something we help buyers navigate every day.

Let's Talk About Your Home Buying StrategyWhen Skipping Points Is the Smarter Move

Just as there's a clear profile for buyers who benefit from points, there's an equally clear profile for buyers who should skip them entirely. This isn't about being risk-averse or financially unsophisticated — it's about reading your situation accurately.

A no-points mortgage is likely the better path when:

- Your timeline is uncertain. Job relocations, growing families, life changes — if there's a meaningful chance you'll move within 5-7 years, paying points is a gamble you're likely to lose. The DFW market has historically seen strong appreciation, which means many buyers sell sooner than they expected when equity builds quickly. Don't lock up cash in points if you might not be around long enough to benefit.

- You're a first-time buyer with limited reserves. The first year of homeownership is expensive in ways that are hard to predict. Appliances break. HVAC systems need service. You realize you need window treatments, a fence, or landscaping. Having cash available for these realities is often more valuable than a slightly lower monthly payment.

- You're buying in a market where refinancing is likely. If rates are significantly above historical norms and there's a reasonable expectation they'll decline, many buyers plan to refinance within 2-3 years. In that scenario, paying points on your current loan is money you'll never recoup.

- The break-even period exceeds 7 years. Some lenders quote rate reductions that are smaller than the standard 0.25% per point, which extends the break-even period significantly. If your break-even calculation comes out to 8, 9, or 10 years, you'd need exceptional certainty about your long-term plans to justify the upfront cost.

- You have higher-interest debt. If you're carrying credit card debt at 18-24% interest, using $4,000-$8,000 to pay down that debt will almost certainly generate a better return than buying down a mortgage rate by 0.25-0.50%.

⚠️ Watch Out for This Common Lender Pitch

Some lenders frame points as a "no-brainer" without ever mentioning the break-even timeline. They'll show you the lower rate and the lower monthly payment and let you draw your own conclusions. If a lender isn't proactively walking you through the break-even analysis, ask for it directly. Any reputable lender should be able to show you exactly how many months it takes to recoup the cost of buying points — and if they can't or won't, that tells you something important about how they operate.

Seller-Paid Points: A Strategy Many DFW Buyers Are Missing

Here's something that doesn't get nearly enough attention in the standard points conversation: you don't always have to pay for points yourself.

In a negotiated real estate transaction, sellers can offer concessions — money credited toward the buyer's closing costs. In many cases, those concessions can be used to buy down the buyer's interest rate. This is called a seller-paid rate buydown, and in certain market conditions, it's a powerful negotiating tool.

The way it typically works: instead of asking the seller to reduce the purchase price by $8,000, you ask them to contribute $8,000 toward your closing costs, specifically to buy down your rate. For the seller, the net effect is similar — they're netting $8,000 less from the sale. But for you, the buyer, the benefit is a lower interest rate for the life of the loan rather than a slightly lower purchase price that gets folded into a larger mortgage anyway.

💡 Why a Rate Buydown Can Beat a Price Reduction

Consider this: if a seller reduces the price by $8,000 on a $400,000 home, your loan becomes $392,000. At 7.00%, your monthly payment drops by about $53. But if that same $8,000 buys down your rate from 7.00% to 6.50%, your monthly payment drops by $133 on the original $400,000 loan. Over 10 years, the rate buydown saves you roughly $9,600 more than the price reduction — and that's before accounting for the fact that a lower purchase price also means lower property taxes in some jurisdictions. The math often favors the buydown, particularly on higher loan amounts.

In the DFW market, where home prices have remained elevated and sellers are increasingly motivated to close deals, asking for seller-paid points is a legitimate and often successful negotiating strategy. It's worth discussing with your real estate agent before you make an offer, because structuring the request correctly matters — both for the negotiation and for lender compliance with contribution limits.

Temporary Buydowns: A Third Option Worth Understanding

Beyond the standard permanent rate buydown (which is what we've been discussing throughout this article), there's another structure called a temporary buydown that has gained popularity in recent years — particularly in markets where buyers are stretched by high rates and sellers want to make deals happen.

The most common version is called a 2-1 buydown. Here's how it works:

- Year 1: Your rate is reduced by 2% below the note rate (so a 7.00% loan becomes 5.00% for the first year)

- Year 2: Your rate is reduced by 1% below the note rate (7.00% becomes 6.00%)

- Year 3 and beyond: You pay the full note rate of 7.00%

The cost of a 2-1 buydown is typically paid by the seller or builder as a concession, and it's held in an escrow account that subsidizes your payments during the buydown period. The appeal is obvious: lower payments in the early years when cash flow is tightest, with the expectation that your income will grow or rates will drop before the full rate kicks in.

📋 Temporary vs. Permanent Buydown: Key Differences

A permanent buydown (standard discount points) lowers your rate for the entire life of the loan. A temporary buydown lowers your rate for 1-3 years and then resets to the full note rate. Permanent buydowns are paid by the buyer at closing; temporary buydowns are typically funded by the seller or builder. If you're comparing offers, make sure you understand which type of buydown is being offered — they have very different long-term implications for your monthly payment and total interest paid.

The risk with a 2-1 buydown is what happens in year 3 when the full rate kicks in. If your income hasn't increased and rates haven't dropped enough to make refinancing worthwhile, you could face a payment shock that strains your budget. Temporary buydowns can be a smart tool, but they require honest planning about what your financial picture will look like when the subsidy ends.

Weighing a temporary buydown offer from a builder or seller? Before you accept, it helps to understand exactly what your payment looks like in year 3 — and whether the numbers still work for your budget.

Get a Straight Answer on Your Buydown OfferHow to Run Your Own Break-Even Analysis in 5 Minutes

You don't need a financial calculator or a spreadsheet to do this. Here's a simple process you can follow with any loan estimate in front of you.

- Find the cost of the points. Look at your loan estimate under "Loan Costs" or "Origination Charges." Discount points will be listed there with a dollar amount. This is your upfront cost.

- Calculate the monthly payment difference. Ask your lender for the monthly principal and interest payment at the rate with points and the rate without points. Subtract the lower number from the higher number. This is your monthly savings.

- Divide upfront cost by monthly savings. That number is your break-even in months. Divide by 12 to get years.

- Compare to your realistic timeline. How long do you genuinely expect to stay in this home with this loan? Be honest. If the break-even is 60 months and you're pretty confident you'll be there for 10 years, buying points looks reasonable. If you're uncertain, lean toward no points.

- Factor in your cash position. After paying the points, how much do you have left in reserves? If the answer is "not much," that's important information. A lower rate doesn't help you if a $3,000 repair puts you in financial stress six months after closing.

That's it. Five steps. The math isn't complicated — it's just rarely explained clearly. And once you've run it yourself, you'll be able to have a much more informed conversation with your lender about what actually makes sense for your situation.

Points and the DFW Real Estate Market: What Local Buyers Should Know

The Dallas-Fort Worth market has its own dynamics that affect how the points decision plays out in practice. A few things worth keeping in mind as a local buyer:

Loan amounts are significant. The median home price in the DFW area has remained well above $350,000 even as the market has moderated from its 2022 peak. On loans of $350,000 to $500,000, the dollar impact of points — both the upfront cost and the monthly savings — is meaningfully larger than on a $200,000 loan. That cuts both ways: the savings are bigger, but so is the risk if you don't stay long enough to recoup.

New construction is abundant. DFW has one of the most active new construction markets in the country, and builders regularly offer rate buydowns as incentives. These are often temporary 2-1 buydowns funded by the builder, and they can look extremely attractive on paper. Make sure you understand what happens when the buydown period ends and whether the underlying note rate is competitive with what you'd get from a third-party lender.

Mobility is high. The DFW metro is one of the fastest-growing in the country, which means the population is relatively transient — people move here for jobs, and they move away for jobs. If you're relocating for work and there's any chance your company could move you again in 3-5 years, that's a critical variable in your break-even analysis.

Property taxes are a significant cost. Texas has no state income tax, but property taxes are among the highest in the nation. DFW buyers often focus so much on the mortgage rate that they underestimate the property tax burden, which can be 2-3% of assessed value annually. Make sure your total housing cost analysis includes taxes and insurance, not just principal and interest — and that buying points doesn't crowd out your ability to handle the full picture.

Frequently Asked Questions: Points vs. No Points Mortgage

The standard benchmark is approximately 0.25% rate reduction per point, but lenders vary. Some offer 0.125% per point, which significantly extends your break-even timeline and makes points much less attractive. The best way to evaluate this is to get quotes from at least two or three lenders and compare both the no-points rate and the cost-per-point reduction across each. If one lender is offering a smaller rate reduction per point than others, that's a sign their pricing isn't competitive. Always ask for the loan estimate in writing so you can compare apples to apples.

Generally, no — discount points are a closing cost that must be paid at closing, not financed into the loan balance. However, there are situations where seller concessions or lender credits can offset the cost of points, which effectively reduces your out-of-pocket expense without you having to pay them directly. Some loan programs also allow gift funds to be used for closing costs, which could include points. If cash at closing is the constraint, discuss with your lender whether seller-paid concessions or other creative structures could make points more accessible for your situation.

The money you paid for points is gone — it does not transfer to a new loan or get refunded. This is the core risk of buying points: if you refinance or sell before reaching your break-even month, you've paid for a benefit you didn't fully receive. This is exactly why the break-even analysis is so important before you commit. If there's a reasonable chance you'll refinance within 5-7 years — whether because rates drop, your financial situation changes, or you want to tap equity — the no-points path protects you from this outcome.

In many cases, yes — but the rules matter. For a primary residence purchase, the IRS generally allows you to deduct discount points in the year they're paid, provided the loan is used to buy or build your main home and the points are within the normal range for your area. For refinances, the deduction is typically spread over the life of the loan rather than taken all at once. Investment properties follow different rules. Because tax situations are individual and the rules have nuances, it's worth confirming with a CPA or tax advisor before factoring the deduction into your break-even calculation.

You can buy points on FHA and VA loans, and the break-even analysis works the same way. However, there are a few additional considerations. FHA loans already carry mortgage insurance premiums (MIP) that add to your monthly cost, so the effective savings from a lower rate are somewhat diluted by that fixed cost. VA loans don't require mortgage insurance, which makes the monthly savings from a lower rate more impactful. In both cases, the key question remains the same: how long will you keep this loan, and do you have the cash reserves to pay points without compromising your financial stability after closing?

It's uncommon and usually not advantageous for most buyers. Most lenders cap the rate reduction at a certain level regardless of how many points you buy, and the returns diminish as you add more points. Additionally, lenders have limits on how low they can set a rate through discount points under certain loan programs. Beyond the structural limits, paying three or more points upfront represents a very large cash outlay — $12,000+ on a $400,000 loan — that most buyers can't absorb without compromising their reserves. If you're seriously considering more than two points, it's worth getting an independent second opinion on whether the math actually supports it for your specific situation.

Let's Run the Real Numbers for Your Mortgage Decision

The points vs. no-points decision isn't one-size-fits-all — it depends on your loan amount, your timeline, your cash position, and what you're actually being offered. If you're trying to figure out whether buying points makes sense for your specific situation in the DFW area, we're happy to walk through the numbers with you, no pressure and no sales pitch. We'll help you see the full picture so you can move forward with confidence.

Let's Look at the Numbers TogetherCheck out this article next